When your estate reaches a level of complexity that includes business interests, real estate holdings, and multi-generational wealth goals, a standard life insurance policy is no longer enough on its own. Without the right legal structure, life insurance proceeds can be pulled directly into your taxable estate, inflating its value and exposing your beneficiaries to significant federal estate tax liability at the worst possible time. For high-net-worth individuals in Texas, an irrevocable life insurance trust offers a proven, legally sound strategy to keep those proceeds outside your estate and in the hands of the people you intend to protect.

At Quadros, Migl & Kilmer, we work with business owners, private equity clients, and real estate investors who need estate planning strategies tailored to the scale and complexity of their businesses. As a boutique firm with offices in Houston, The Woodlands, Dallas, and Austin, our attorneys bring over 60 years of combined legal experience to comprehensive, cost-effective, client-first planning that integrates your personal and business interests into a cohesive whole.

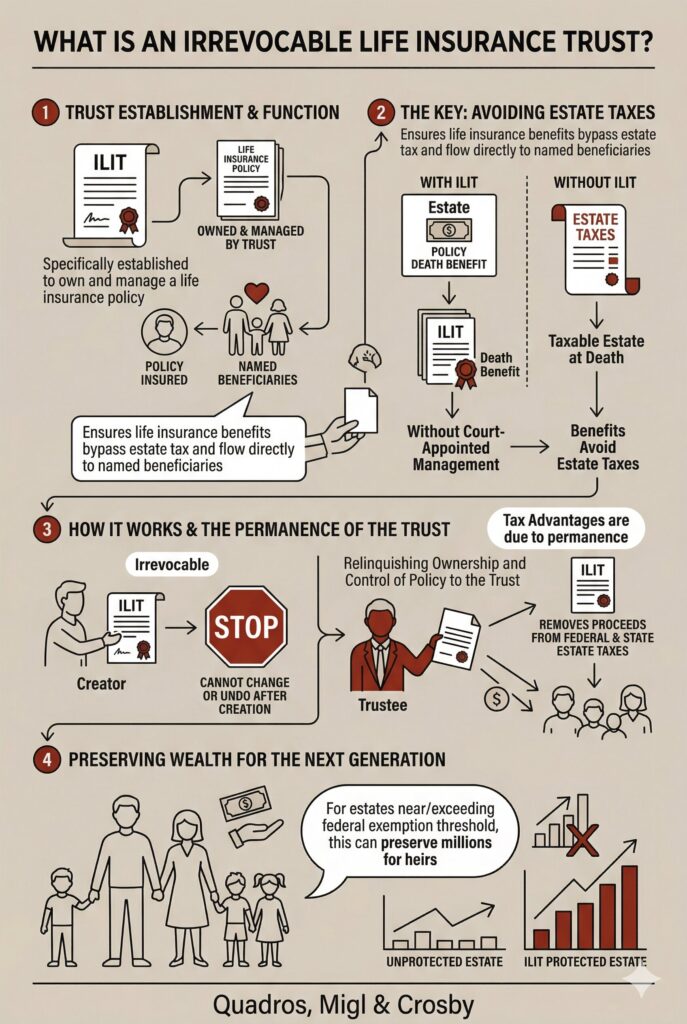

What Is an Irrevocable Life Insurance Trust?

An irrevocable life insurance trust, commonly referred to as an ILIT, is a trust established specifically to own and manage a life insurance policy on behalf of named beneficiaries. Because the trust owns the policy rather than the insured, the death benefit is not considered part of the insured’s taxable estate at death. According to the Legal Information Institute at Cornell Law School, ILITs allow individuals to ensure life insurance benefits avoid estate taxes and follow the interests of the insured, and because the trust is irrevocable by nature, the insured cannot change or undo it after creation.

That permanence is precisely what gives an ILIT its tax advantages. By relinquishing ownership and control of the policy to the trust, the insured removes the proceeds from the reach of both federal and, where applicable, state estate taxes. For estates approaching or exceeding the federal exemption threshold, this distinction can mean millions of dollars preserved for the next generation.

The Core Tax Benefits of an ILIT

For high-net-worth individuals, the tax advantages of an ILIT extend across several dimensions of estate planning. When considering your estate planning options, it is important to understand what an ILIT can and cannot do before deciding whether it belongs in your plan. The primary tax benefits most clients seek include:

- Estate tax exclusion: Because the ILIT owns the policy, the death benefit is excluded from the insured’s gross estate, potentially saving millions in federal estate taxes for large estates.

- Gift tax management: Premium payments to the ILIT are treated as gifts to the beneficiaries, and when structured correctly using Crummey notices, those gifts can qualify for the annual gift tax exclusion.

- Generation-skipping transfer planning: ILITs can be structured to pass wealth to grandchildren or future generations while minimizing exposure to the generation-skipping transfer tax.

- Income tax-free proceeds: Life insurance death benefits paid to the trust are generally received by the trust and its beneficiaries income tax-free.

Each of these benefits requires careful drafting and ongoing administration to remain intact, which is why working with an attorney who understands both trust law and tax strategy is critical.

Why ILITs Matter for Business Owners and Investors

For Texas business owners and real estate investors, an ILIT serves purposes well beyond personal estate tax savings. Business succession planning often involves life insurance as a funding mechanism for buy-sell agreements, key person coverage, or liquidity at death. When those policies are held inside an ILIT, the proceeds remain outside the estate while still being available to meet business obligations. Clients with complex corporate finance needs or multi-layered ownership structures often find that an ILIT becomes a core component of a coordinated wealth transfer strategy.

This is especially valuable for clients whose estates include illiquid holdings. Investors with significant Texas real estate assets held through an LLC benefit from the liquidity an ILIT-held policy can provide at death, giving heirs the cash needed to maintain holdings rather than liquidate them under pressure.

Important Considerations When Establishing an ILIT

An ILIT requires careful planning and ongoing administration to maintain its tax benefits. The three-year rule under federal law means that a policy transferred to an ILIT within three years of the insured’s death may still be included in the taxable estate, so establishing the trust before acquiring a new policy is generally preferred. Additionally, Crummey notices must be sent to beneficiaries each time a premium payment is made to ensure the contribution qualifies for the annual gift tax exclusion. These procedural requirements are not optional and are what keep the ILIT legally intact and tax-efficient over time.

Contact Quadros, Migl & Kilmer for Sophisticated Estate Planning

Our estate planning practice has deep experience in complex trust structures, wealth transfer planning, and business succession strategies for high-net-worth clients across Texas. We take a comprehensive approach, connecting the dots between your personal estate, your business interests, and your long-term goals to build plans that are both strategic and durable.

If you are ready to explore whether an ILIT belongs in your estate plan, we invite you to connect with our team. Reach out to Quadros, Migl & Kilmer today through our online contact form to schedule a consultation at our offices in Houston, The Woodlands, Dallas, or Austin.