You have spent decades building a business, and the day you have been planning for is finally approaching: a sale, a transition, or a transfer of significant assets. How you structure that transfer can dramatically affect how much of your wealth you actually keep, give, and pass on. For business owners sitting on highly appreciated assets, a charitable remainder trust (CRT) may be one of the most powerful planning tools available.

At Quadros, Migl & Kilmer, we understand that estate planning for business owners is rarely straightforward. You are not just managing personal wealth; you are navigating business interests, real estate holdings, family considerations, and tax exposure all at once. With over 60 years of combined legal experience, our attorneys are uniquely equipped to help business owners throughout Houston, The Woodlands, Dallas, and Austin evaluate whether a charitable remainder trust belongs in their broader estate and exit strategy.

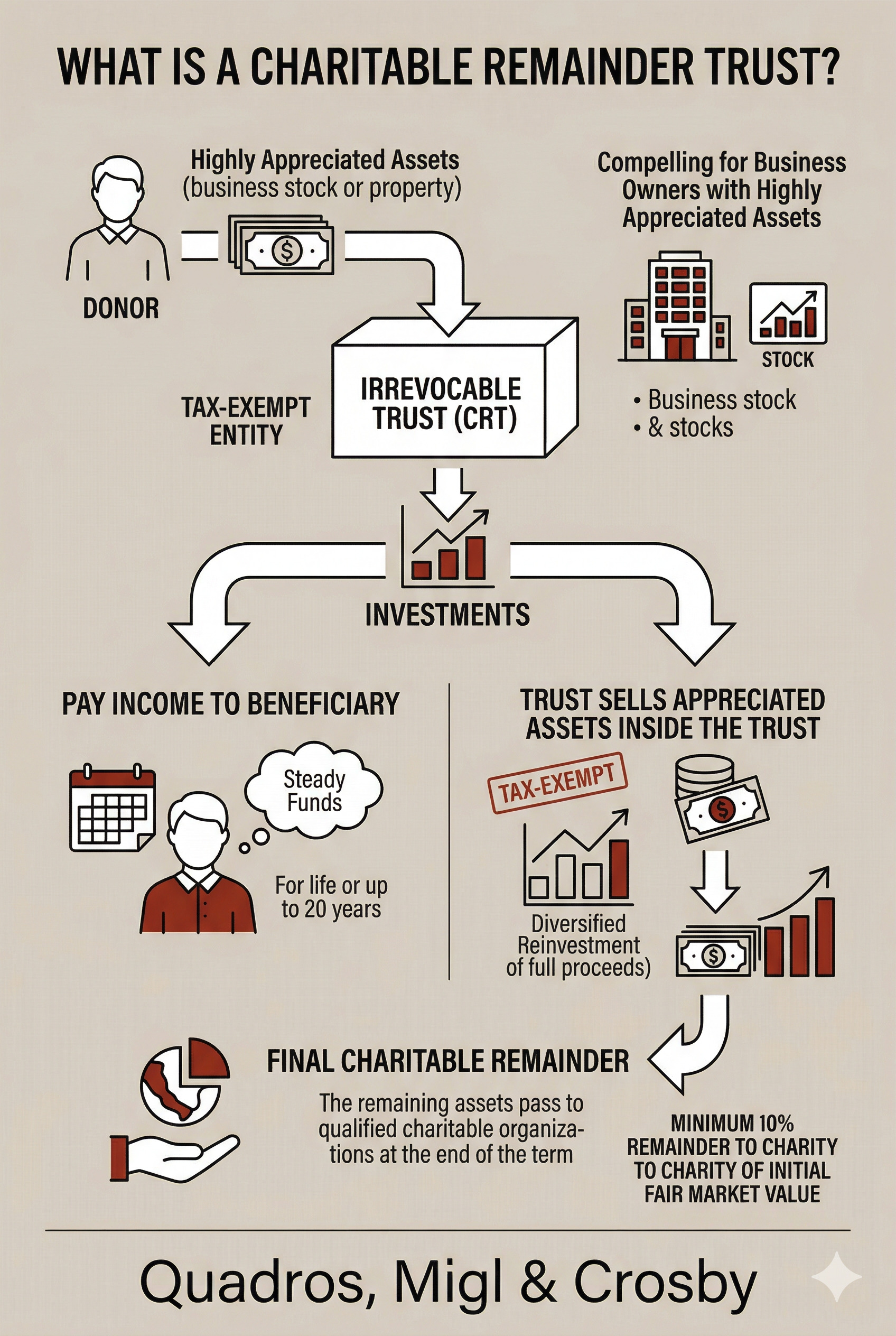

What Is a Charitable Remainder Trust?

A charitable remainder trust is an irrevocable trust into which you transfer assets. According to the IRS, the trust pays income to at least one living beneficiary for a specific term of up to 20 years or for the life of one or more beneficiaries, and at the end of that period, the remaining assets pass to one or more qualified charitable organizations. The charitable remainder must equal at least 10% of the initial net fair market value of all property placed in the trust.

For business owners, this structure is particularly compelling when you hold highly appreciated assets you want to diversify without immediately triggering a substantial capital gains tax bill. Because the CRT itself is a tax-exempt entity, it can sell appreciated assets inside the trust without recognizing gain at the time of the sale, allowing the full proceeds to be reinvested and generating a larger income stream than if you had sold and paid taxes first.

Two Types of Charitable Remainder Trusts

There are two primary forms of charitable remainder trusts, and the right structure depends on your financial goals. A charitable remainder annuity trust (CRAT) pays a fixed dollar amount each year, providing predictable, stable income regardless of investment performance. A charitable remainder unitrust (CRUT) pays a fixed percentage of the trust’s assets as revalued each year, meaning your income can grow over time if investments perform well. The following factors are typically at the center of this choice:

- Income stability: A CRAT is the better fit if you need consistent, predictable distributions year after year.

- Growth potential: A CRUT may be preferable if you want distributions that can increase with investment performance.

- Asset flexibility: A CRUT generally allows for additional contributions after the trust is established, while a CRAT does not.

- Tax deduction timing: Both structures provide a partial charitable deduction in the year the trust is funded, based on the present value of the charitable remainder interest.

Understanding which structure aligns with your goals requires careful coordination between your legal and financial advisors.

When Does a CRT Make Sense for Business Owners?

Not every business owner will benefit from a charitable remainder trust, but there are specific circumstances in which the strategy is especially valuable.

You Are Planning a Business Sale

If you are preparing to sell a business or a significant business interest, a CRT can allow you to transfer appreciated assets into the trust before the sale closes. The trust, rather than you personally, can then complete the sale, deferring capital gains tax and preserving more proceeds to generate income over time. This approach works naturally alongside mergers and acquisitions planning and should be evaluated well in advance of any transaction.

You Hold Appreciated Commercial Real Estate

Business owners who hold appreciated commercial real estate face the same capital gains challenges as those selling a business. Transferring property into a CRT before a sale can defer recognition of gain, provide a charitable deduction, and generate ongoing income, all while reducing the taxable value of your estate. Coordinating with a corporate finance attorney early in the process makes a meaningful difference in outcomes.

You Have Charitable Goals Alongside Wealth Transfer Goals

If philanthropy is already part of your financial picture, a CRT allows you to benefit from assets during your lifetime while ensuring your chosen charitable beneficiaries receive a meaningful gift. This type of planning often works in tandem with your business organization and your ultimately exit plan.

Important Limitations to Understand

A charitable remainder trust is irrevocable. Once assets are transferred in, they cannot be taken back, making thoughtful drafting and structuring essential before any assets are committed to the trust. The income you receive is also taxable, classified as ordinary income, capital gains, and then corpus distributions. For business owners with complex entity structures, evaluating how a CRT interacts with buy-sell agreements and succession planning is equally important before moving forward.

Work With Quadros, Migl & Kilmer on Your Estate and Exit Planning

At Quadros, Migl & Kilmer, our estate planning attorney, Jennifer Murray, brings deep experience working with business owners on complex estate and exit planning matters. She understands that your business and personal finances are not separate, and her ability to coordinate across real estate, business transfers, and broader planning needs sets our firm apart from a generic estate planning practice. We provide cost-effective, client-first, practical legal solutions to business owners throughout Texas who need more than a one-size-fits-all approach.

If you are approaching a business sale, holding appreciated assets, or simply want to understand whether a charitable remainder trust belongs in your plan, we invite you to connect with our team. Contact us today to schedule a consultation and take the first step toward a more strategic and tax-efficient approach to your estate planning.